This Country Is Leading The Way In Sustainable Steel Manufacturing

Steel is the skeleton of the modern world. From the skyscrapers defining our skylines to the cars in our driveways and the appliances in our kitchens, our lives are forged in steel.

As a fundamental raw material industry, steel is the largest carbon emitter among all 31 manufacturing sub-sectors, consuming 7% of global energy and pumping out 9% of global carbon dioxide emissions.

A groundbreaking new study published in Scientific Reports takes a massive swing at answering the question of whether the steel industry can become more sustainable.

Focusing on the 64 countries along the "Belt and Road Initiative" (BRI)—a region that produced a staggering 1.43 billion tons of crude steel in 2024, or 75.8% of the global output—researchers have developed a new way to measure sustainability.

Researchers at Beijing Technology and Business University first developed a new model for measuring the impacts of the steel industry called the ESG-MI model. It stands for Environmental, Social, and Governance and they added Mineral Resources extraction (M) and Industrial base (I).

How Sustainable is the Steel Industry?

If you look at the big picture, the news is cautiously optimistic. Over the last two decades, the sustainability level of the steel industry along the Belt and Road has shown a steady upward trend.

Between 2000 and 2023, the overall Sustainable Development Index (SDI) rose from 11 to 14, growing at an average rate of 1.04% per year.

But when you peel back the layers, a stark divide appears. The growth wasn't fueled by becoming "greener." It was fueled by becoming "better governed" and "more industrialized."

The Governance score skyrocketed by 65.1%, and the Industry score grew by 58.5%. This means countries are getting better at regulating the industry and building stronger factories. The Social score grew modestly by 13.3%, and the Resource score by 25.3%. But, the Environmental score actually dropped by 10.5%.

The steel industry is becoming more robust and better managed, but it is struggling to reduce its environmental footprint. The resource supply chain also proved to be incredibly fragile; during the 2009 financial crisis, the resource index plummeted by 16.0%, showing how vulnerable these countries are to external shocks.

The Winners and Losers

Not all countries are created equal when it comes to steel. The study ranked 64 countries, revealing massive disparities.

The Heavyweight Champion: China

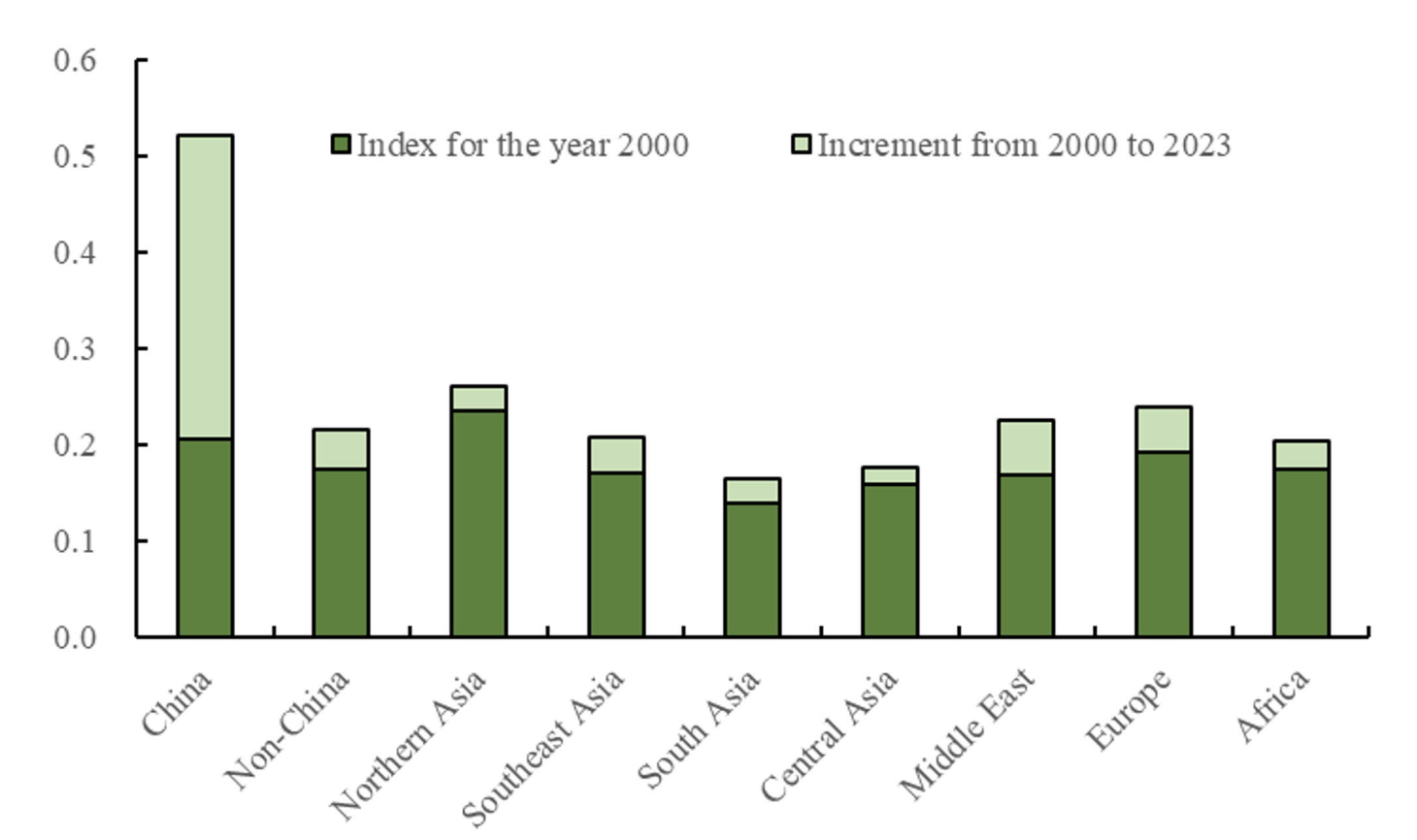

SDI of the steel industry in China and different regions along the belt and road in 2000 and 2023

China is in a league of its own. In 2023, China’s SDI score hit 0.520, which is ranking first among all regions. For context, that is 2.3 times higher than the average level along the Belt and Road. China’s index grew by a staggering 154.3% from 2000 to 2023.

Why? The study points to a "triple advantage" of policy, investment, and technology. Since launching the "Steel Industry Adjustment and Revitalization Plan" in 2009 and the "Ultra-Low Emissions Retrofit Plan" in 2019, China has aggressively pushed for cleaner production and outdated capacity elimination.

Top Performers

Joining China at the top are countries like Bahrain, Slovakia, Russia, the UAE, and the Czech Republic. These nations have managed to balance industrial output with better governance and resource management.

The Strugglers

At the bottom of the list are Yemen, Afghanistan, Syria, and Turkmenistan. Yemen and Afghanistan, in particular, face severe challenges. Political instability and war have halted industrial modernization.

For example, Yemen has no industry standards for energy conservation, and factories in Afghanistan rely on manual processes and outdated equipment that consumes huge amounts of energy for very little output.

Barriers to Sustainable Steel

If we want green steel, what is standing in our way? The researchers used an "Obstacle Degree Model" to identify the biggest barriers.

Surprisingly, the biggest hurdle isn't just "pollution"—it's the structure of the industry itself.

Industrial Value Added

This is the single biggest barrier, with a massive obstacle score of 19 in 2023. This suggests that for many countries, the steel industry isn't generating enough economic value relative to its size and impact. It’s "big" but not "efficient" or "high-value."

Crude Steel Output Per Capita: High production volumes per person create massive resource strain.

Proportion of Ores and Metals in Exports: Many of these countries are stuck in the role of raw material exporters rather than high-tech manufacturers.

Since 2000 the industry has shifted from having issues with weak infrastructure and lack of education to ecological pressure and governance challenges.

Now, the industry is trapped in a cycle of needing more resources to fuel inefficient factories.

The Path to Green Steel

The study doesn't just point out problems; it offers a roadmap for the future. The Belt and Road region is critical because it holds 61.5% of the world's population and includes some of the most dynamic economies. If steel goes green here, it goes green globally.

The Tech Fix: Hydrogen and Scrap

The traditional way of making steel involves burning coal to strip oxygen from iron ore. This is dirty. The study highlights Hydrogen Metallurgy as a key solution. This involves using hydrogen instead of coal, emitting water vapor instead of CO2. China is already investing heavily in this, along with electric arc furnaces that melt down scrap metal instead of mining new ore30.

“Recycling 1 kg of scrap steel saves 1.5 kg of CO2 emissions and 1.4 kg of iron ore.”

Regional Cooperation

Pollution doesn't respect borders. The study suggests a "Hydrogen Metallurgy Pilot Country Cooperation Framework". Countries with advanced tech (like China) need to share standards and technology with lagging regions (like Central Asia).

The "Scrap" Economy

We need a better system for trading recycled steel. Establish a regional cooperation mechanism for scrap steel recycling to ensure these valuable resources circulate efficiently rather than rusting in landfills.

ESG Transparency

Governments need to force companies to show their cards. By integrating ESG performance into government procurement and financing, companies will be financially motivated to clean up their act.

As the Belt and Road region continues to industrialize, the old model of "pollute first, clean up later" is hitting a wall. The shift from infrastructure barriers to ecological barriers proves that we have solved the easy problems. Now, we must solve the hard ones.

With China leading the way in policy and technology, there is a blueprint for success. But for the global steel industry to truly become sustainable, it requires a massive shift toward high-value manufacturing, hydrogen technology, and a circular economy where old steel becomes new steel, again and again.